Stay-at Home Parents & Healthcare

Employer-sponsored health care is good, actually. But it could be better for families with a breadwinner and a homemaker.

As many readers of this Substack know, I write frequently about families with a stay-at-home parent. For families that have one parent at home and the other in the workforce, health insurance coverage is a major problem. To understand this problem, we need to talk a bit about how the United States provides healthcare to most of its workers.

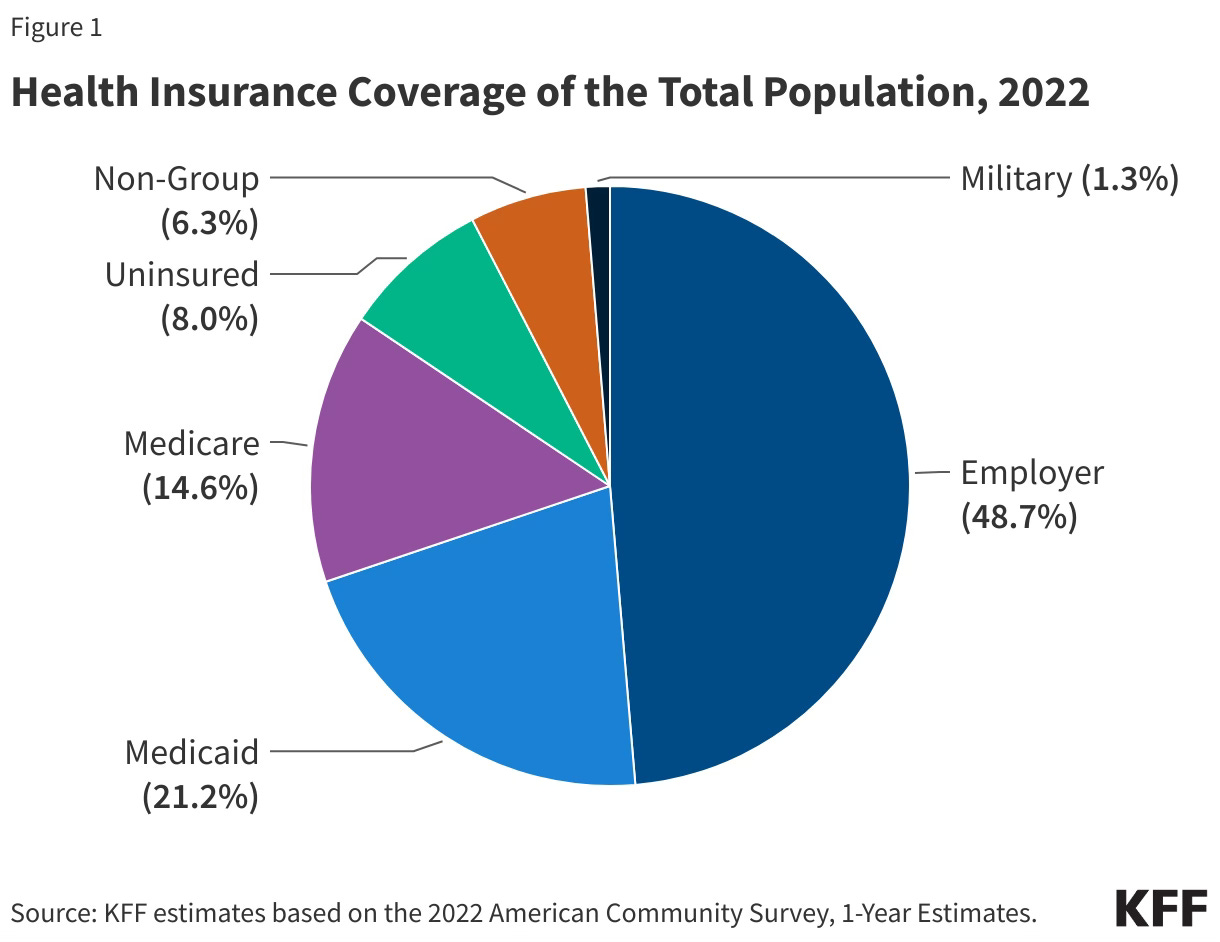

Instead of paying for healthcare directly (like countries that have socialized healthcare), the U.S. federal government gives significant tax breaks to employers that offer health coverage. Through the Affordable Care Act (“ACA”), the federal government also mandates some employer coverage. As a result, the most common way an adult working full-time in the U.S. gets health care is through “employer-sponsored healthcare,” or health insurance a worker gets from the company he or she works for.

One of my most heterodox policy opinions is that some kinds of employer-sponsored healthcare are actually very good. I can think of certain institutions where holding such an opinion would get you consigned to Antarctica, but I do hold it!

If you have good employer-sponsored health insurance in the United States, you have access to some of the very best health care in the world. This is why, for example, many retirees fight to stay on their employer plans after retirement (even though they usually have access to Medicare at that point, which is also fairly good health care). Retiree health benefits are dying out, but they’re still a very valuable perk for those that have access to them.

Popular media often describes the U.S. as a weird outlier in its reliance on employer-sponsored health plans. However, a number of other countries are similar to the United States in that their working-age populations are also covered by a mix of public health care and employer-sponsored health plans. This doesn’t mean that health coverage in those countries works exactly like it does in the United States. In France, for example, the state provides minimum health coverage, and then employers are required to offer (and help pay for) supplemental coverage. Still, the United States is certainly not alone in relying significantly on employers to provide medical insurance to workers … and, as I said previously, our good employer-sponsored health insurance is actually very good.

In a best case scenario, employers compete with each other to provide excellent health insurance to recruit and retain their workforce. Companies also can help negotiate with insurance companies and health care providers on behalf of their employees (a task the average person probably finds daunting!) In my opinion, the problem is not that we rely on employer health coverage. The issue is that many people aren’t covered by these plans, or are covered by a bad plan — and these are particularly serious problems for families with a breadwinner/homemaker division of labor.

First, many families with a stay-at-home parent simply aren’t covered by employer insurance. A recent viral post on X drew attention to this problem:

For these families, there are a number of reasons why they can’t get employer-sponsored coverage. Like the post on X quoted above, sometimes the breadwinner is an entrepreneur. Sometimes the breadwinner works for a small business that isn’t required to — and doesn’t — offer health insurance. These families usually can look for insurance on the Affordable Care Act exchanges, but that can be very, very expensive. The last time I looked, premium rates for families that weren’t eligible for government subsidies were well over $2,000 per month … for health insurance with significant copays and deductibles. Subsidies can help families below a certain income level afford coverage on the ACA exchanges, to be sure. This is a new development: in the past families with a homemaker usually weren’t eligible for these subsidies due to a problem called the “Family Glitch.” That glitch has now been fixed, but at least one analyst is trying to convince the incoming Congress and President to walk back the fix! Even without the “Family Glitch,” the system isn’t perfect, and many families fall through the gaps for one reason or another.

Second, sometimes employer-sponsored health care for families simply isn’t very good or is too expensive. As I discuss in this paper, employers often subsidize health insurance for individuals more than they subsidize family health insurance, so it ends up being very expensive for breadwinners with a big family to take advantage of their company healthcare. Or, as this fantastic new paper by the think-tank EPPC points out, the offered employer benefits don’t sufficiently cover medical costs incurred by families — instead making families pay large copays and deductibles for things like childbirth. To fix this problem, some have argued that employers should be required to cover 100% of pregnancy and childbirth costs so that families aren’t left with big medical bills after the birth of a new baby.

There are few issues as important to families with a stay-at-home parent than the cost of health coverage. We don’t have comprehensive proposed solutions. Indeed, we don’t even yet have wide-spread recognition of the scope of the problem. The incoming Congress and new Administration will more than have their work cut out for them should they choose to seriously tackle family healthcare issues — and it’s not clear that they’re interested in doing that.

If you have a story or complaint about this issue (or an idea to try to fix it) I’d love to hear about it.

My husband is an icu nurse and during Covid he began to feel “trapped” because of the need to stay employed to keep the health insurance benefits for our young family. We didn’t want that to be the case, so we switched to a medical sharing ministry and dropped the insurance entirely. It’s worked so great for us, and I believe it’s such a better and healthier (emotionally) option.

Glad to see you writing about this! It is a necessary and underexplored topic. I know a couple of women, including my mother in law, who continued working at jobs they hated instead of staying home because their husband owned a small business and needed their healthcare benefits.

I live in a military town in NC with one of the top birth rates in the country…There are obviously a host of factors at play but I always wonder how much of it has to do with the healthcare.

https://www.statista.com/statistics/432838/us-metropolitan-areas-with-the-highest-birth-rate/

(After looking at the list again I realize a lot of the towns are military.)